U.S. Department of Transportation

Federal Highway Administration

1200 New Jersey Avenue, SE

Washington, DC 20590

202-366-4000

The 12-member scan team of audit and financial management specialists visited five European countries that have extensive experience in highway construction using public-private partnerships. Government officials from the audit agencies and road transport agencies of Portugal, Spain, France, England, and Ireland welcomed the U.S. team and presented information on (1) audit practices, both external and internal, (2) stewardship of the government's assets, (3) oversight of large road projects, many of which were accomplished through public-private partnerships, and (4) the use of tolls and concession contracts in meeting service needs of multiple constituencies. The scan team's observations of the audit environment in the five host countries are provided in this chapter so that readers can more fully appreciate the findings and recommendation presented in the next chapter.

All five counties visited are members of the European Union. Membership gives broad economic advantages, including free trade between members, an option for a single currency, virtual removal of border crossings, and removal of barriers for banking and commerce transactions. EU membership does require members to adhere to certain mandated economic policies. The Maastricht Treaty has established debt limits and annual deficit limits for members. A nation's overall debt limit cannot exceed 60 percent of its GDP. In addition, the annual deficit of a nation must be below 3 percent. These are very stringent guides for many EU members. In fact, based on the last national budget approved by the U.S. Congress, the United States would be out of compliance with the requirements for EU membership.

The European Union, collectively, is integrating members' transportation systems into a seamless EU "interstate" road and rail system. The cost of this venture is significant and increasing. The host countries the scan team visited all have ambitious long-range and short-range transportation programs underway. New motorways, bridges, tunnels, and road infrastructure construction were visible throughout the team's tour.

Debt and deficit limitations have led to new methods of financing transportation infrastructure off balance sheet (neither assets nor debt reported by the state and assigned to the private partner). Private financing has been encouraged by the European Union and road projects are prime areas for private financing. Design-build-finance with concessions, design-build-maintain with concessions, and design-build-finance-maintain-and-operate with concessions are all project schemes that could lend themselves to classification under the general heading of a PPP. All of these project schemes could have private financing. These PPP projects have a relatively long and accepted history among EU members.

Public-private partnership with private financing and concessions is readily used for road projects. Concessions can be either conventional with real tolling or shadow tolling. Real tolling charges the actual user of the road for the service and convenience of that respective highway, tunnel, or bridge. User charges normally are set to recover the cost of the road project and maintain the predetermined operating condition of that road and are high enough to allow for the private partner's profit. Shadow tolling, on the other hand, has the appearance of a free road because there is no charge to the actual user of the road. Instead, the government uses other general revenue streams to pay for the cost of the project and the annual maintenance. These shadow tolls are included in the elements of a public-private partnership contract that cover construction, operation, maintenance, and private sector profits. They are paid from current and future revenues. As several European hosts stated, "There is no such thing as a free road."

Tolling of major motorways, however, is common throughout the European Union and appears to be tolerated by European citizens as a proper means to finance roads. In other words, EU citizens are not averse to paying a toll for a road that meets quality and safety expectations and provides travel time savings compared to an alternate, lower-quality free route. In addition to accepting road, tunnel, and bridge tolls as a cost of travel, EU citizens also do not seem to have an aversion to private ownership of public infrastructure as a normal way of doing business. These observations are collective, and the scan team observed varying degrees of acceptance in the countries it visited.

European citizens' acceptance of the use of PPPs and tolling concessions might be attributable to the government's commitment to its stewardship responsibilities for public assets. As the experience level has risen, EU countries have restricted the length of PPP contracts to 21 to 35 years rather than 75 to 99 years. This corresponds with the accepted lengths of government bonds, commercial mortgages, and reasonable risk assessments. In addition, several countries include review and renegotiation of payments every 7.5 years to prevent private partners from earning "super profits" from a government contract.

|

Super profits are profits earned on a PPP contract that are more than could be earned in the private sector, given the same risk environment. |

Another component used in concession contracts is availability payments, which are made to the private sector partner during maintenance work when a predetermined number of lanes are available to roadway users. When lanes are not available and traffic congestion or stoppage occurs, the availability payment is not made. Although this is a penalty for the private sector partner, it is also a shadow toll because the government is making payments for lane availability. All European hosts indicated that they were trying to move away from shadow tolling to a more transparent cost for establishing tollway user charges.

Private roads and ferries were common in the United States during the 18th and 19th centuries. They fell out of use as the Federal and local governments began to develop transportation infrastructure during the 20th century. Today, the United States once again is considering private ownership of highway infrastructure projects using PPPs and concessions. At the January 2006 Transportation Research Board meeting, speaker Brian Grote stated that "FHWA is in the early stages of a paradigm shift. That shift is negligible in relation to the billions annually spent on our Nation's roads, but nevertheless a shift to private financing. The use of a PPP for major road projects is underway." He then cited the Chicago Skyway, the Indiana Tollway, and Texas and California projects as just the beginning.

Why now in the United States? According to AASHTO Executive Director John Horsley, "The shortfall in gasoline tax revenues of $7 billion to meet the annual highway transportation needs is a driving force. It appears that the U.S. is embracing PPP with concessions in order to meet its current and future highway transportation needs. Tolling for quality (safety, time, and gasoline savings) roads is becoming increasingly more acceptable to the U.S. drivers. This also shifts the cost of the roads to the users." The transportation newsletter Innovation Briefs, in a follow-up to a February 2006 commentary on highway tolling, reported that in March and May 2006 there were 16 new toll projects under study in States "across this nation. PPP and tolling are becoming the jargon most often heard among highway folks." It appears that major transportation systems, because of lack of highway funds, will have to be accomplished with private financing with concessions or basically with PPPs. While this concept of innovative financing with PPPs is relatively new in the United States, it has gone through an evolutionary process in Europe and much can be learned from Europe's mistakes and successes.

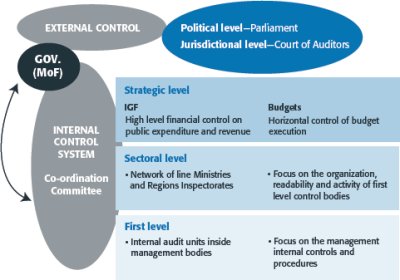

Team members gained valuable insights into audit practices during their meetings with European independent and internal auditors. The responsibility for the independent audit function in the host countries rests primarily with the central government. This is similar to the U.S. model in which each State, like a European nation-state, uses its own audit agency to conduct the independent (financial statement) audit function rather than the Government Accountability Office (GAO). All host countries visited had both independent and internal auditing agencies. The independent audit agency was responsible primarily for the financial audit functions and displayed independence from the executive branch of government by answering to Parliament, similar to the U.S. Federal model with the GAO answering to the U.S. Congress. In one country, Portugal, the audit function was located in the Ministry of Finance, but had oversight by Parliament (see figure 1).

The responsibility (organizational placement) for the internal audit function in the host countries visited was similar to internal audit organization placement in the United States. The internal audit function resides in each agency and/or ministry of the country. In the United States, the internal audit function is placed in each agency of the State or Federal government.

Figure 1: An EU example of audit authority structure

Source: Inspector General Office, Ministry of Finance, Republic of Portugal

Independent and internal audit services were similar to those offered in the United States. The work of the independent European auditors includes financial audits, attestation engagements (audit of various management assertions and representations), and performance audits (service efforts and accomplishment reporting). European internal audit agencies often provide management advisory services and audits of economy, efficiency, and effectiveness of operations similar to those offered in the United States. Although independent audit emphasis is on financial statement auditing, auditors also perform financial, compliance, internal control, project, management assertion, and various performance audits, not unlike the United States. The European internal audit agencies are called on regularly to offer consulting services (advisory services) to agencies within their ministry. They are considered a management resource providing expertise in operational, financial, and control engagements.

Audit standards are quality guides used in conducting an audit. Audit procedures and practices are the actions (the work elements) performed by an auditor to gather evidence to corroborate or refute the management representations being investigated (audited).

Audit standards are "broad statements of auditors' responsibilities. They promise a framework for assuring that the auditors have the competence, integrity, objectivity, and independence in conducting and reporting their work."(2) |

European independent (financial statement) audit standards are known as International Standards on Auditing (ISAs) and are issued by the International Auditing and Assurance Standards Board (IAASB) of the International Federation of Accountants (IFAC). These standards are not usually cited in auditing materials printed for the U.S. market. However, the ISAs, with minor exceptions, closely parallel the U.S. audit standards promulgated by the American Institute of Certified Public Accountants (AICPA) and now the Public Companies Accounting Oversight Board (PCAOB).

The International Organization of Supreme Audit Institutions (INTOSAI) was created by the United Nations to issue governmental auditing standards applicable to all public sector organizations throughout the world. European auditors follow INTOSAI governmental auditing standards. The government audits in the United States follow generally accepted government audit standards (GAGAS) promulgated by the GAO. European internal audit standards, including performance audits, are generally based on standards issued by the Institute of Internal Auditors, headquartered in Altamonte Springs, Florida. Internal auditors in the United States use these internal audit standards or GAGAS.

The scan team members observed that European standards, practices, and terminology for auditing are similar to those in the United States. Little difference exists in the knowledge, skills, and abilities required to practice internal or external auditing in the European Union and the United States.

Generally accepted accounting principles (GAAP) are promulgated by several different authoritative bodies. Once readers of financial statements understand the rules or guides, they are able to interpret and analyze any organization's representations (financial reports) prepared according to GAAP. GAAP for U.S. for-profit corporations and not-for-profit organizations are promulgated by the Financial Accounting Standards Board (FASB). The Governmental Accounting Standards Board (GASB), an independent not-for-profit organization, establishes financial reporting standards for U.S. State and local governments. The U.S. Government establishes its own GAAP through an advisory board known as Federal Accounting Standards Advisory Board (FASAB). State governments, therefore, follow GASB, which requires full accrual reporting, while the Federal government follows FASAB, which is moving to a full accrual reporting basis.

Generally accepted accounting principles are authoritative guidance to be followed in the preparation of an organization's basic financial statements. |

There are differences between U.S. GAAP and international GAAP. For a trained accountant, the differences are easily reconcilable. National governments in Europe, like the U.S. Government, maintain and follow their respective methodologies for preparing financial statements. Each government's legislative body establishes financial reporting standards for European governments. Several countries follow International Accounting Standards (IAS) issued by the International Accounting Standards Committee (IASC) of the International Accounting Standards Board (IASB). The basis of accounting for measurement and financial reporting among host countries visited ranges from cash basis to full accrual basis. The European Union allows differences in financial reporting requirements between member states, but it does have certain requirements for recording budgetary expenditures and reporting national debt.

The agency's chief executive officer (CEO) is often called a department head. The head of the department of transportation is also commonly referred to as the agency accountability officer in England and the agency accounting officer in Ireland. These titles are given to agency CEOs to emphasize their responsibility for all financial dealings, internal control procedures, and "representations" of their departments. To assure the CEO that the country's PPP policy, laws, regulations, accounting controls, financial reporting, procurement laws, and EU requirements are being followed, several host countries have established a distinct position of process auditor. A process auditor is a person selected by the CEO to monitor the RFP preparation and selection process to assure the CEO of total compliance with all laws, procedures, and practices.

Audit stewardship includes practices before contract initiation. These practices set the financial and performance objectives and prepare the business model before the adoption of a capital project. In the United States, auditors, internal or independent, are rarely involved with the initial stages of a highway construction project. The auditors typically become involved in a project at the various stages of partial contract payments and when the project is completed.

|

A business model is a business plan, a clearly written document that identifies the business, its products, its goals, and its objectives. A plan is developed for each capital investment and includes, but is not limited to, goals, objectives, cost, financing, and expected return (financial, social, risk analysis, and expected contribution to the overall organization). A business plan should incorporate robust financial analysis using present value and internal rate of return techniques. |

In the European host countries visited, the procurement process involves a team of qualified personnel with finance, audit, and legal credentials. The team convenes at the beginning of the capital investment highway construction planning process and follows the project through to completion and operation. If needed, the team also can include contract consultants with specific expertise. The team develops business models using extensive risk analysis, capital budgeting techniques, and sensitivity analysis (what-if analysis) to help in project selection and RFP development.

PPPs with concessions require robust business plans/models to evaluate project selection and proposals. Generally, traffic counts are an integral part of a concession contract bid. The Europeans have found it helpful to use an independent party to develop the traffic counts for the government to use to assure consistency in the evaluation of bid contract proposals. Contract proposals are reviewed by finance and audit personnel. Total project costs are developed using present value and internal rate-of-return techniques to establish a capital project value. These techniques, internal rate of return (IRR) and present value (PV), are also used in the project business modeling plan and bid selection process.

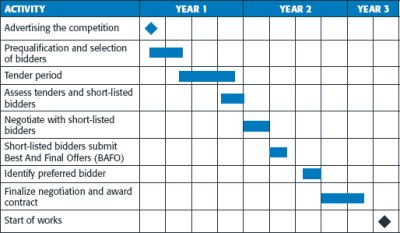

Project delivery, in the European host countries, is affected by the size of the project, type of financing arrangements, and elements of the contract. In Europe, major projects generally are defined as greater than $14 million and are carried out under some type of design-build (DB) process, including design-build-finance-operate (DBFO) and design-build-operate-maintain (DBOM), rather than the design-bid-build model (DBB) that is the U.S. standard. This causes a longer project development period (see figure 2), but usually results in a project that is on time and on budget.

All host countries have developed PPP capital project practices for planning, project selection, developing an RFP, reviewing tenders and tender selection, and developing performance measures to monitor implementation and project delivery. Practices during contract and post-contract periods involve the evaluation of work performed, use of project costing standards, distribution of profits from concessions, compliance with contract provisions, and an evaluation of overall price and quality of services received.

Figure 2: Illustration of a procurement process

Source: Inspector General Office, Ministry of Finance, Republic of Portugal

International host countries emphasized that oversight is best accomplished through clear, concise, and complete contract terms. Most European countries have an experienced planning team composed of qualified financial, legal, engineering, and management experts for large projects with concessions. This group is involved with the determination and quantification of the contract risk, contract objectives, and performance objectives. These three elements–contract risk, contract objectives, and performance objectives–will become the framework for the audit program within the project life cycle.

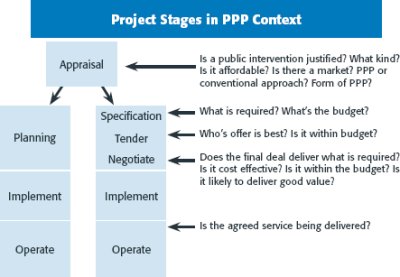

Throughout the host countries, the scan team observed an emphasis on capital project selection, analysis, approval, and implementation. This process is illustrated in figure 3.

Figure 3: Illustration of project stages in a PPP

Source: Office of the Comptroller and Auditor General, Ireland

The extent and depth of process can be illustrated by a summary of the Guidelines for the Appraisal and Management of Capital Expenditure Proposals in the Public Sector, issued by the Department of Finance in Ireland in 2005:

There are four stages of project appraisal and management: (1) appraisal, (2) planning/approval, (3) implementation, and (4) post-project review. It is not a detailed planning and cost control hand book. Instead, it sets out the main steps which should be followed in evaluating and managing capital expenditure projects, considers the major issues of principle involved, and describes the principal methods of appraisal.

Generally, there are two types of toll projects: user tolls or shadow tolls (taxation). A user toll occurs when the toll road operator charges the user of the road for services and not the general taxpayers who may or may not use the road. Shadow tolls are hidden tolls paid to the private partner (concessionaire) from general tax revenues. The concessionaire receives a set amount for each vehicle that uses the road network based on a predetermined rate per vehicle type or a fixed amount for keeping a motorway lane open. Therefore, when shadow tolls are used, they are in fact only a methodology of earmarking current and future taxes to finance a road project. The conclusion to draw from this financing reality is that there are no free roads, only a choice of who pays.

The value of the payments for the shadow toll per type of vehicle is established during the initial phase of PPP formation. Verification of road or bridge usage and resulting payments is readily available in real time to both the government and the private partner. The country with the largest use of shadow tolls was Portugal. However, the headline of the lead article in the November 2004 TOLLROADSnews read, "'Portugal to toll all motorways—free roads no longer financially viable'...Finance Minister." Like other European host countries, shadow tolling appears to have fallen out of favor and Portugal plans to convert all shadow toll concessions to real toll concessions. During their presentations, the host country representatives outlined currently operating DBFO projects that use shadow tolls. They also stated reasons, both financial and social (a fairness issue concerning who pays tolls for roads and who does not), for not using them in the future. Private financing of roads and bridges paid with shadow tolls does not free up tax revenues for other projects. To summarize, the European host countries were all reevaluating the use of shadow tolls because of a fairness concern and budget constraints.

Concession and private transportation operations (PPP) are widely used today in the European Union. Until recently, the few toll roads in the United States were not in private hands, but were owned by public corporations or public authorities. With the recent leases of the Chicago Skyway and the Indiana Tollway, private ownership with concessions is an indicator of the possible direction for future funding of U.S. highway transportation projects. Collectively, new construction projects by the international host countries are funded about 50 percent by concessions and are classified as PPPs. Each host country has developed an extensive road construction plan that includes private financing with concessions.

The scan team also found that the terms in PPP and concession contracts have a myriad of elements, depending on the nature of the specific contract. Each PPP with concessions is unique regarding ownership, type of concession, risk, financing, contract length, and elements of project delivery. Nontraditional projects such as public-private partnerships (DBOM and/or DBFO) may be more costly than traditional projects such as DBBs. As financing risk is shifted to the private sector, the financing costs of highway projects may increase because of private sector financing. The private sector expects a return (profit) on its private investment. In the European Union, the private sector expects a return of 7 to 17 percent on its investment. Life cycle costs are generally not considered in DBB or DBFO contracts in the United States. However, life cycle costs become an integral part of the PPP project evaluation in the countries the scan team visited. In Ireland, value for money and whole life costing (life cycle costing) become central to the evaluation and selection of all capital spending proposals. Delivering large infrastructure projects is complex and requires a constant review and adjustment, if necessary, of concession payment mechanisms, bid procedures, project size, and tolling risk. The PPP mechanism requires varied expertise from the auditors whose role is to safeguard the public interest.

PPP profits should be limited to a reasonable return for the private partner. A number of European countries identified concessionaires earning super profits as a result of PPP contracts. Super profits are profits that excessively exceed the expected rate of return in comparison to the concessionaire's initial proposal. Charges of a PPP earning a super profit must be determined on a case-by-case approach. The host countries indicated that profit-sharing models with PPPs should be structured on revenue generated rather than profits earned because revenues can be more easily monitored and audited. Several host countries stated that in future PPP contracts they plan to add a contract clause that would allow a review of the concession contract clauses every 7.5 years. The review would allow the government to renegotiate profit-sharing arrangements and concession profit levels in general.

PPP profit projections are closely related to financing terms outlined in the original project proposal and profit expectations outlined in the contract. When interest rates change, refinancing of debt could mean an immediate windfall profit for the private sector PPP partner. Host countries recognize that financing terms in the initial contract proposal can have future changes that drastically change the profit structure. Host countries include a clause in PPP contracts that requires a sharing of any refinancing profits. Several host countries require an equal share of any and all refinancing profits. This refinancing sharing arrangement is detailed in the original tender (bid) specifications.

| << Previous | Contents | Next >> |