U.S. Department of Transportation

Federal Highway Administration

1200 New Jersey Avenue, SE

Washington, DC 20590

202-366-4000

Over a 2-week period, scan team members visited five host countries in Europe and met with transportation officials, auditors, accountants, and financial executives. The purpose of the scan was to gather information on audit stewardship and oversight practices employed by the host EU countries. The host countries chosen for the scan had years of experience dealing with a variety of PPPs (DBM, DBOM, DBFO, financed privately with concessions) on large and innovative highway transportation projects. This fact was confirmed beginning with the scan team's first meeting in Portugal and continued throughout the meetings in all host countries. The European countries visited had extensive experience with PPPs and other nontraditional vehicles for delivering road infrastructure assets.

The EU goal of having seamless major motorway transportation systems throughout the European Union had caused a significant increase in highway construction. These ambitious motorway construction plans led not only to private sector financing but also to new delivery methods of PPPs. Contracts for PPPs with concession and financing arrangements have been an evolutionary process in the host countries. This is clearly demonstrated by the differences between the terms of initial (early stage) PPP contracts and those now being planned and developed. The countries explained their increasing use of business models and project evaluations as well as the sophisticated stewardship and oversight processes they conducted.

The scan team is aware that not all best practices identified in the EU host countries are transferable to U.S. highway programs in identical or even modified form. Political, social, and economic systems differ from country to country. What may work for one government may not be applicable to another. In addition, the scan team is aware that some of the best practices it identified may already have been implemented fully or in a modified manner in one or more of the 50 State highway programs. The scan team believes that the best practices discussed in this chapter have merit for analysis and possible implementation in the audit stewardship and oversight area of the many PPP programs being considered in the United States. The findings and recommendations are presented in three categories: audit stewardship, audit oversight, and general audit issues.

Audit stewardship Includes audit practices before contract initiation, including how financial evaluations are made to obtain the best outcome for the funds invested, how the government can receive the best value for the public, whether the proposing company has the resources to perform the project, evaluation of proposal costs, the sale and valuation of State assets, and audit reporting methods used to advise agencies on the mitigation of risk in the event of project difficulties.

The first finding and recommendation in the stewardship category could have been put into any one of the three categories, but it was placed under stewardship because of its importance. All five host countries emphasized the lack of and need for new auditor tools and skills. In fact, Ireland's Interdepartmental Group on Public-Private Partnerships issued a white paper titled "Framework for PPP Awareness and Training." Ireland patterns its training program for PPP after that of the United Kingdom. The United Kingdom experience was evolutionary and identified a variety of skills needed so that public sector employees can effectively approve, monitor, and evaluate PPP projects.

Portugal, England, France, Ireland, and Spain all addressed the employee skill sets necessary for dealing with new and innovative finance initiatives and the various and complex PPP models. All countries now use a diverse team approach in which team members have accounting, auditing, engineering, business modeling, financial analysis, capital budgeting, legal, and negotiation skills. These skills were identified as necessary for government teams to stand as equals with the private sector business teams that submit proposals and negotiate for private ownership with concessions for infrastructure of traditional public assets. These teams are convened at the initial planning stages of any proposed project and remain until delivery and final project evaluation. When expertise is lacking, new team members with required skills are added. The government also can hire private sector consultants if in-house personnel lack the required skill sets.

England and Ireland have established a new position of process auditor to monitor PPP initiatives through the tender (bid) process. Ireland's process auditor performs the "function of recording the completion of a number of processes in a PPP project, including the Stakeholder Consultation process. In the event that the Process Auditor has a concern of a material nature in the process, there are a number of actions available to him/her as set out in the detailed Process Auditor Guidelines. The process auditor is appointed by the Agency Head and is answerable directly to the chief executive officer (CEO)." (See sample procurement process checklist in Appendix F.)

Audit stewardship is achieved during the planning process of major innovative finance projects or PPPs. Audit review is ongoing throughout the life of the project. Clear performance objectives should be developed for each stage of the PPP life cycle, along with audit monitoring methodology to appraise the performance objectives. Public sector comparators (comparables) need to be developed early in the initial planning stage.

|

Public sector comparators (comparables) provide a realistic estimate of how much it would cost the public sector to provide the identified transportation project. The standard of design quality to be achieved should be clearly demonstrated, including how the project expectations can be met within an agreed affordability envelope. |

The goals of a PPP include speedy and cost-efficient value for money projects using private financing arrangements with concessions to allow transportation agencies to meet the increased demand for efficient, safe, and quality highways without increases in general or gasoline tax revenues. At the heart of audit stewardship is assurance that corporate governance is followed.

For it is through governance that an organization achieves its objectives and targets. It is about establishing a framework of control that supports innovation, integrity, and accountability, and encourages good management throughout the organization. (May 16, 2006, presentation to scan team in England)

Each host country had a team or organization, usually within the national ministry of finance, that developed policies and controls for use with PPP capital procurement projects. In Ireland, the National Development Finance Agency was responsible for this function. Created by legislation, its main functions are to (1) advise state authorities on optimal means of financing public investment projects, (2) advance moneys if necessary, (3) provide advice on financing public investment, and (4) establish (when necessary) special purpose companies.

All host countries emphasized that PPP contracts should be clear and concise with specific clauses dealing with (1) concessions and sharing of concession profits with the government if toll revenues (concession) exceed initial projections, (2) future increases in toll charges by the concessionaire, (3) the sharing arrangement with the government if super profits occur in an amount well beyond initial expectations detailed in the business plan used to create and award the PPP contract, and (4) the sharing of profits from refinancing debt. All of the host countries recognized that PPPs are a financing mechanism and that the interest rate in the tender is subject to market fluctuation. Therefore, they expect to keep the rate of return for private partners reasonable by requiring them to share any refinancing profits. Contracts should be clearly written to avoid or prevent future contract litigation. A contract clause, in case of disputes, should require binding arbitration.

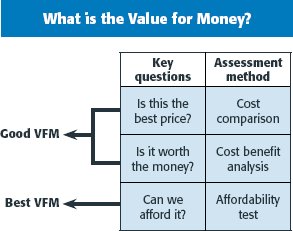

Figure 4: Value for money

Source: Office of the Comptroller and Auditor General, Ireland

When PPPs were being implemented throughout the European Union, contracts were commonly written for 60 to 99 years. The host country representatives stated that earlier PPP contract lives were excessive and that current and future PPP contracts are limited to 30 to 35 years. A host country representative explained the 30-to-35-year contract limitation in relatively simple terms: "If a PPP is a financing arrangement, then the PPP contract period should be no longer than the length of a typical financing instrument used to finance similar assets."

England and France plan to introduce a renegotiation clause in PPP contracts at the end of each 7.5 years. This 7.5-year clause would allow all concession items to be renegotiated throughout the contract life.

Audit oversight-Includes audit practices during contract and post-contract periods involving the evaluation of work performed, use of project costing standards, distribution of profits from concessions, compliance with contract provisions, and an evaluation of overall price and quality of services received.

Host countries encouraged the development of a viable business plan as a condition for the effective control of a PPP capital highway project. The business plan outlines the project scope, objectives, alternative project, comparables, risk, time line, and necessary elements to develop a bid or tender. This business plan will present the VFM analysis and all elements that will become the foundation for development of life cycle audit objectives. Auditors and finance personnel need to be involved early in the process, providing a consultative role.

PPPs with concessions involve complex issues of economic revenue projections and monitoring and auditing of toll collections by the private sector. A PPP should be used only if it can be justified from a business sense. A PPP with concessions can release State DOT funds for use for necessary traditional transportation projects. The private financing for the PPP project is, of course, a business venture. Therefore, the public sector should use robust business modeling, including the same tools private business uses to determine capital investment selection and return (value for money).

The European governments are moving to transferring risk to private contractors for major projects. The business model developed for each project determines the amount of risk transferred to the contractor. The countries approached the allocation of risk in PPP contracts differently based on their budgets and project requirements. The most appropriate risk allocation basis should be used for each type of contract and project, given the circumstances. However, all host countries agreed that the greater the risk transferred to the private sector, the greater the cost of the project.

The European Union has established a goal for a seamless interstate motorway system to increase commerce within and between the member states. Because of the extensive and different tolling systems throughout the European Union, the host countries showed concern and interest in the development of a seamless EU tolling collection system to facilitate nonstop tolling. Citizens would be able to buy a toll pass and use it throughout the EU states. Centralized billing and/or credit card charges could be processed electronically. Tolling costs would be more transparent to the user and governments would be more accountable for the cost per mile for toll road usage. In addition, auditors would be able to verify toll road usage more easily by sharing traffic counts with neighboring states.

| << Previous | Contents | Next >> |